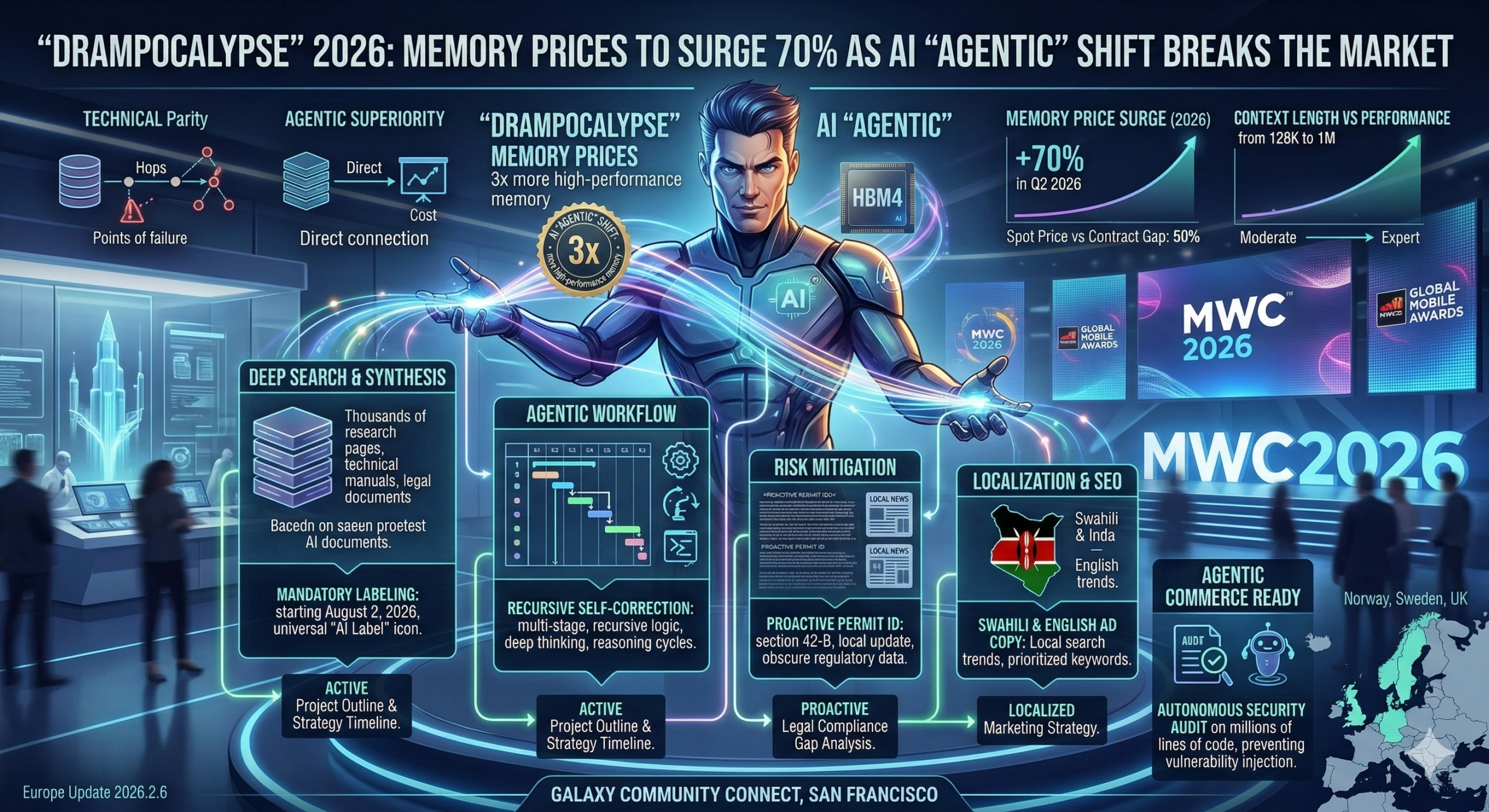

SEOUL / SANTA CLARA — March 9, 2026 — The global semiconductor industry is bracing for a “violent dislocation” in the memory market. Industry leaders Samsung Electronics and SK Hynix have officially notified customers of a second wave of massive price hikes for Q2 2026, with some analysts projecting that DRAM prices will surge by an additional 70% after already doubling in the first quarter.

The crisis is driven by a structural pivot: the transition from simple generative chatbots to “Agentic AI”—autonomous systems that handle planning, reasoning, and multi-app task execution. These agents require up to 3x more high-performance memory than previous models, prompting hyperscalers like Google, Microsoft, and Meta to buy every available chip, regardless of the cost.

Closing the “Gap”: Spot vs. Contract Parity

For the past six months, a massive 50% price gap has existed between “spot” prices (market rates for immediate delivery) and “contract” prices (bulk rates set months in advance). Manufacturers are now moving aggressively to close this gap by resetting quarterly contracts to reflect the new reality.

-

“Take It or Leave It”: Small and mid-sized electronics firms are reportedly facing “hourly pricing” models. Reports indicate that Samsung and SK Hynix are rejecting long-term (2-3 year) agreements in favor of quarterly resets to capture the rising market.

-

Prepayment Required: In an unprecedented shift, suppliers are increasingly demanding cash prepayments or “volume reservations” from non-Big Tech buyers just to secure an allocation for the second half of 2026.

-

Samsung’s 60% Capacity Limit: Industry sources claim Samsung’s current production lines can only meet about 60% of surging DRAM demand, as most of their wafer capacity is being cannibalized to produce high-margin HBM4 (High Bandwidth Memory) for NVIDIA’s new Rubin GPUs.

Cascading Costs: From Fabs to Smartphones

The impact is rapidly moving from the factory floor to the consumer’s pocket. Memory, which traditionally accounted for 15% of a premium smartphone’s build cost, now represents as much as 35%.

| Component / Device | Price Trend (Q2 2026 Projection) | Consumer Impact |

| DDR4 16Gb Spot | +70% to 90% | DIY PC market “vanishing” |

| DDR5 Enterprise | +60% | Server costs doubling |

| LPDDR5X (Mobile) | +100% (Finalized for Apple) | Smartphone ASP to rise by ~$150 |

| Enterprise SSDs | +100% | Cloud storage surcharges expected |

“The bottleneck on AI scaling has migrated,” says a leading industry analyst. “In 2024, the constraint was the GPU. In 2026, it is memory and advanced packaging. We are entering the most violent price dislocation in semiconductor history.”

The “Rubin” Effect: Silicon Cannibalization

The primary culprit for the standard DRAM shortage is HBM4. Each of NVIDIA’s upcoming Rubin (R100) chips requires eight stacks of HBM4, which consumes three times more silicon wafer area than standard DRAM. To meet Jensen Huang’s demand for the Rubin platform, Samsung and SK Hynix are literally taking machines offline that used to make the RAM for your laptops and smartphones.

Gartner and IDC have already revised their 2026 forecasts, predicting a 10% contraction in global PC shipments as manufacturers like Dell and HP are forced to raise prices significantly or delay product launches.

700 701 702 703 704 705 706 707 708 709 710 711 712 713 714 715 716 717 718 719 720 721 722 723 724 725 726 727 728 729 730 731 732 733 734 735 736 737 738 739 740 741 742 743 744 745 746 747 748 749 750 751 752 753 754 755 756 757 758 759 760 761 762 763 764 765 766 767 768 769 770 771 772 773 774 775 776 777 778 779 780 781 782 783 784 785 786 787 788 789 790 791 792 793 794 795 796 797 798 799 800 801 802 803 804 805 806 807 808 809 810 811 812 813 814 815 816 817 818 819 820 821 822